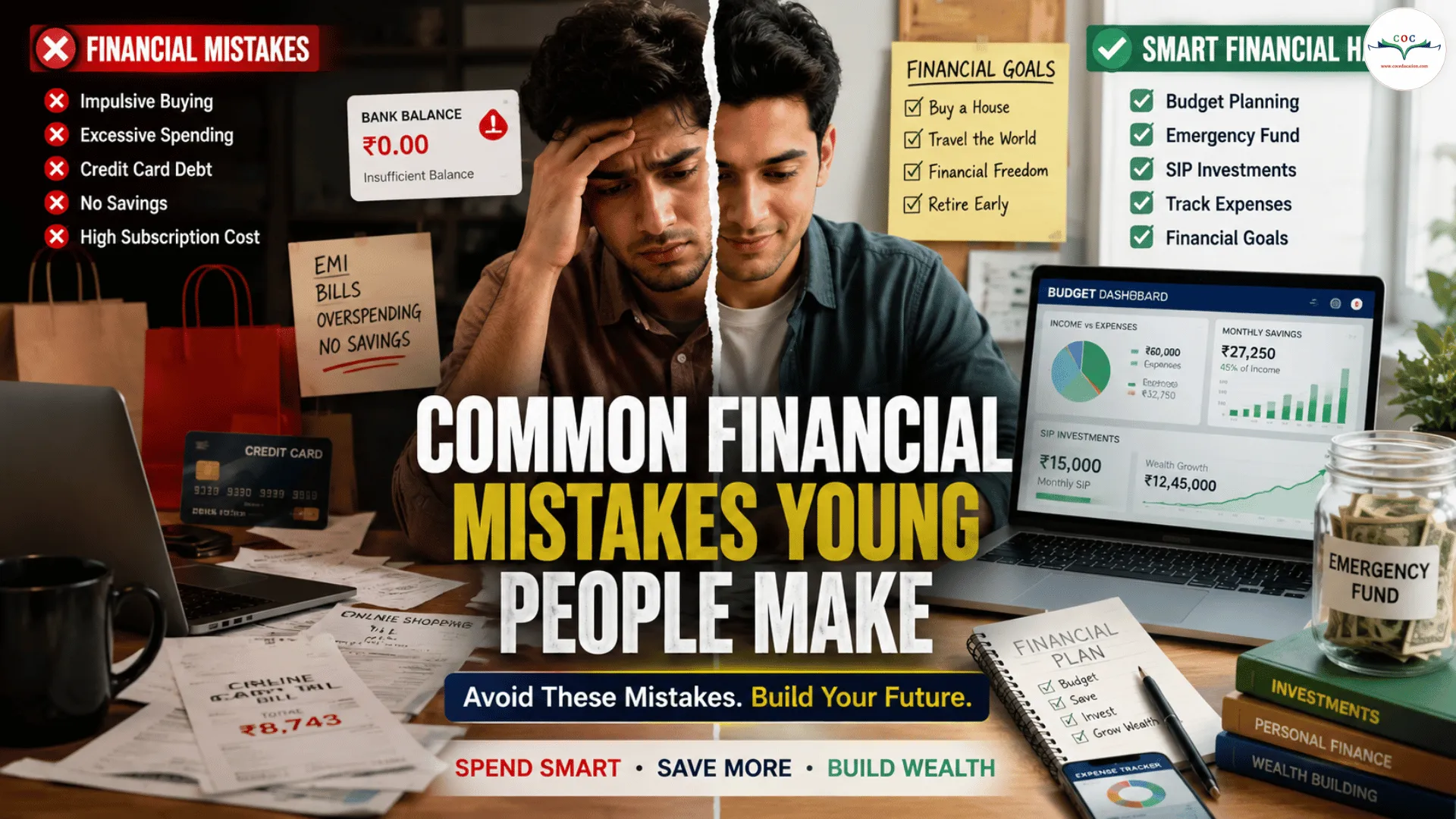

Common Financial Mistakes Young People Make

Common Financial Mistakes Young People Make

Introduction

Managing money is one of the most important life skills, yet many young people start their financial journey without proper guidance. As a result, they often make financial mistakes that can affect their savings, investments, and long-term wealth creation.

The good news is that most of these mistakes are avoidable. By understanding them early, students and young professionals can make smarter financial decisions and build a stronger financial future.

Let's look at some of the most common financial mistakes young people make and how to avoid them.

1. Not Having a Budget

One of the biggest mistakes young earners make is spending money without tracking where it goes.

Many people know how much they earn but have no idea how much they spend every month.

Why It's a Problem

Without a budget:

Expenses become difficult to control

Savings remain inconsistent

Unnecessary spending increases

What You Should Do

Create a simple monthly budget and track:

Income

Fixed expenses

Variable expenses

Savings

Investments

A budget gives you control over your money.

2. Delaying Savings

Many young people believe they can start saving later when their income increases.

Unfortunately, this habit often continues for years.

Why It's a Problem

The biggest advantage young people have is time.

Starting early allows savings to grow through the power of compounding.

What You Should Do

Follow the "Pay Yourself First" principle.

Save a portion of your income before spending on anything else.

3. Ignoring Emergency Funds

Unexpected situations can arise at any time:

Medical emergencies

Job loss

Family emergencies

Urgent repairs

Without an emergency fund, people often rely on loans or credit cards.

What You Should Do

Build an emergency fund covering at least 3–6 months of essential expenses.

This provides financial security during difficult times.

4. Using Credit Cards Carelessly

Credit cards are useful financial tools when used responsibly.

However, many young people treat them as extra income.

Common Mistakes

Overspending

Paying only the minimum amount due

Missing payment deadlines

Consequences

High-interest charges

Debt accumulation

Poor credit score

What You Should Do

Use credit cards only for planned expenses and always pay bills on time.

5. Living Beyond Their Means

Social media often creates pressure to maintain a lifestyle that exceeds one's income.

People spend money on:

Expensive gadgets

Luxury purchases

Frequent dining out

Unnecessary subscriptions

What You Should Do

Focus on your financial goals instead of comparing yourself with others.

A strong financial future is more valuable than temporary appearances.

6. Not Learning About Investments

Many young people keep all their money in savings accounts because they believe investing is risky or complicated.

Why It's a Mistake

Inflation reduces the purchasing power of money over time.

Simply saving is often not enough.

What You Should Do

Start learning about:

Mutual Funds

SIPs

Stocks

Bonds

Retirement Planning

Even small investments can create significant wealth over time.

7. Depending on a Single Source of Income

Relying entirely on one salary can be risky.

Economic changes, layoffs, or industry disruptions can affect income unexpectedly.

What You Should Do

Develop additional income sources such as:

Freelancing

Online skills

Investments

Part-time projects

Multiple income streams improve financial stability.

8. Not Setting Financial Goals

Without goals, it becomes difficult to make smart financial decisions.

Many young people spend first and think about goals later.

Examples of Financial Goals

Buying a house

Higher education

Starting a business

Building retirement wealth

Creating financial freedom

Clear goals help prioritize spending and saving.

9. Avoiding Financial Education

Schools and colleges often focus on academic knowledge but provide limited financial education.

As a result, many people enter adulthood without understanding:

Budgeting

Investing

Taxes

Insurance

Personal finance

What You Should Do

Continuously improve your financial knowledge through books, courses, blogs, and practical learning.

Financial literacy is one of the most valuable skills you can develop.

10. Waiting for the "Perfect Time"

Many people postpone saving, investing, or financial planning because they think they need more money first.

The truth is:

The perfect time rarely arrives.

What You Should Do

Start with what you have today.

Small actions taken consistently often produce better results than waiting for ideal conditions.

Conclusion

Financial success is not determined by how much money you earn. It is determined by how well you manage the money you earn.

Avoiding common financial mistakes can help young people build strong financial habits, reduce stress, and create long-term wealth.

The earlier you learn these lessons, the easier it becomes to achieve financial stability and financial freedom.